Healthcare Guide

The trend towards value-based care continues, requiring suppliers to approach markets differently.

The ballooning costs of [healthcare] act as a hungry tapeworm on the American economy.”

— Warren Buffet, American business magnate

Healthcare spending in the US is double that of other high-income nations,1 potentially crowding out investments in education, infrastructure, and employee wage growth. The numbers are harrowing.

Annual US healthcare spend per individual is now $10,348 (compared to $4,192 in the UK)2. The average 2018 annual health insurance premium for family coverage has exploded to $19,616, outpacing US workers’ wage growth by 2.4% from the previous year.3, 4 Projections indicate that healthcare expenditure growth will eclipse gross domestic product growth at least through 2026, leaving Americans with the burden of spending $1 of every $5 on healthcare.5

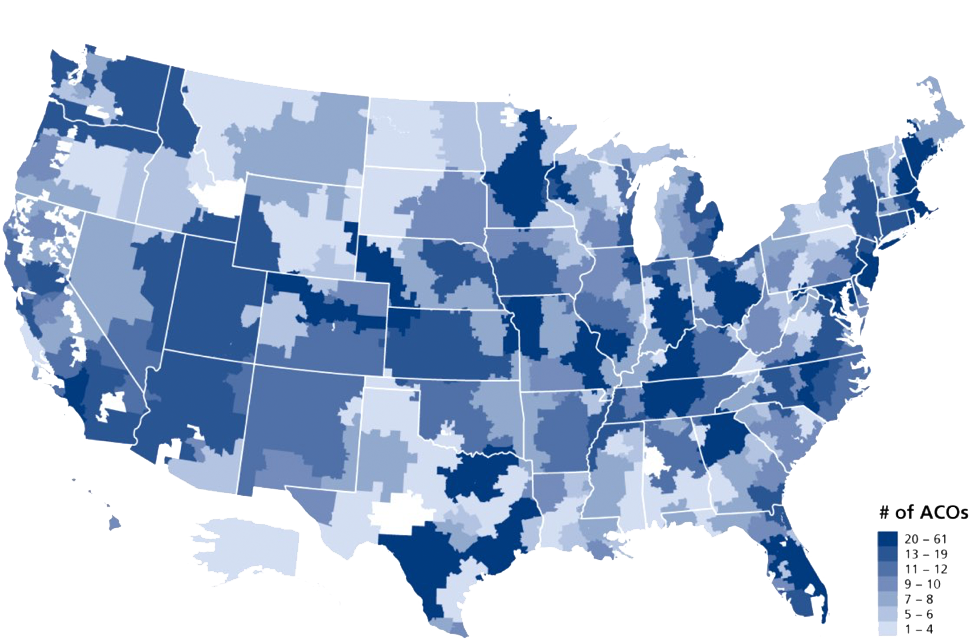

Providers and payers are reorienting care delivery toward value in an effort to bend the cost curve and address runaway costs. Value-based payment models are proliferating across the country, including episode-based bundled payments, patient-centered medical homes, and accountable care organizations (ACOs). As Figure 1 demonstrates, this evolution toward value is complex and variable across markets and even across individual organizations.6

Suppliers are challenged to stay relevant in traditional fee-for-service and progressive, value-based markets at the same time. Those suppliers that deploy the right people supported by well-defined processes and innovative technologies will be best positioned to thrive in this variable and rapidly evolving market.

We are moving, just like the rest of healthcare, to a value-based model, where we get paid in some fashion for actually achieving the outcome. It's a step we have to take to make sure that the value we create with our technologies is truly realized. And when it gets realized, we will get paid fairly for it.” 7

— Omar Ishrak, PhD, Medtronic CEO

As provider consolidation continues, integrated delivery networks (IDNs) play a key role as the enterprise architecting value definition in many markets. While well-recognized IDNs, such as those experimenting with different value-based vehicles, vary in complexity and level of risk, the available opportunity for most suppliers exists in IDNs that are not currently taking on substantial risk but are on the precipice of shifting toward value-based care models in a more meaningful way.

Given that supply chain expense represents 30% of hospital operations — often the second largest cost to these IDNs after labor — the success of any value-based initiative hinges on strategic partnerships with suppliers.8

This requires device vendors to more effectively utilize those resources that help them understand, capture, and quantify real-time market and customer trends the best: field-based representatives. Reps who leverage process-oriented engagement strategies with market-leading field execution, business intelligence, and customer relationship management solutions are able to elevate conversations with providers as trusted advisors.

The data these reps are able to generate using innovative technology solutions support the development of market intelligence and in-depth knowledge of organizations’ strategic objectives. When they execute at a high level, field reps facilitate an improved understanding of how device vendors’ products provide value to these IDNs.

The adaptations suppliers must make vary by market. In taking a more localized approach, device vendors establish strategic partnerships where both providers and suppliers win. These expanded partnerships allow for the formation of new types of business arrangements that include the sharing of resources and expertise. However, to establish this type of relationship, an in-depth understanding of real-time market conditions and organizational positioning derived from field-based reps using innovative approaches and tools is required.

The partnerships described above were formed through various means; however, at the core of each is a vendor that brings unique capabilities and market knowledge to further the goals of an IDN. These goals may be accomplished through the utilization of data. Over time, vendors that are able to provide data-derived insights can evolve the nature of their partnerships with IDNs from transactional to ongoing valued partnerships that provide the foundation for multiple purchases and co-development opportunities. To establish this type of partnership, though, vendors must be well positioned to offer insights and services that are valuable to IDNs and differentiate vendors from the capabilities of IDNs and their vendor competitors.

Today, only a minority of US markets are fully value oriented to value-based care, with only 32% of the population in leading markets for accountability and value readiness (Figure 3). Yet forward progress toward value continues. The transition to value is experiencing an uneven rate of progress, with some markets moving faster than others. This variability between markets means that market stratification has begun. For suppliers, market variation impacts the success of traditional representative access models, as providers, payers and employers in value-leading markets begin to shift their expectations from suppliers and redefine rules of engagement.

Additionally, despite several efforts to reduce supply expenses, studies show that the majority of hospitals can reduce these costs further, by an average of $11 million annually. Increasingly, health systems are looking to their supplier relationships to continue moving the needle on supply-related costs. In particular, IDNs are becoming more refined and diligent at tracking the impact that medical devices have on health outcomes, utilizing sophisticated data analytics, and holding suppliers accountable for the guarantees made at the point of sale.

While the pace of movement toward value is variable, forward momentum will continue as commercial payers, progressive providers, and other key stakeholders in the market ecosystem tackle rising costs (Figure 2). As this trend continues, suppliers need to approach markets differently and adopt field-based strategies that foster deeper, more meaningful partnerships.

Schedule a live demo with a product expert to see how GoSpotCheck’s field execution management platform can transform your business.

Schedule a Demo

Read our case studies or white papers to learn more about how GoSpotCheck enables field teams to optimize for effective data collection and reporting.

A library of case studies with real-world examples of how our customers leverage GoSpotCheck.

Read On ›Our extensive library of white papers has information and guidance tailored to your industry.

Start Exploring ›These markets are largely categorized by their advanced Systems of CARE. While these markets are highly competitive, consolidation may occur in them as it does frequently in others. Additionally, these markets are able to benefit from improved alignment between payers and providers, with employers becoming involved as well. Finally, these markets frequently feature IDNs, which participate in government innovation programs such as the CMS Bundled Payment Program.

These markets also contain organizations that are committed to value-based care, but they have experienced minimal action to date. While significant building efforts to expand Systems of CARE and the presence of preliminary risk models are emerging, they are not highly prevalent. Finally, these markets feature IDNs and stakeholders in general who are seeking to learn from stakeholders with more experience in risk and clinical integration. These markets are generally simply learning how to work across stakeholders.

These are segmented by their minimal interest in evolving value-based care business models that do not have a proven financial return. These markets have limited scale available to them, lack local government support, and experience a higher for-profit presence than other markets. These markets are plagued by disconnected Systems of CARE and limited cooperation by stakeholders.

Note: This article was written in collaboration with Sg2, a vendor-neutral strategy advisory consulting firm that helps healthcare organizations integrate, prioritize, and drive growth and performance across the continuum of care. The opinions expressed in this article are those of GoSpotCheck, and do not reflect an endorsement by Sg2.